The principle behind legislative oversight of executive activity is to ensure that public policy is administered in accordance with legislative intent, and by inference, the citizens’ aspirations. With the advent of devolution in Kenya, our county assemblies were handed the role of scrutinizing the budget estimates from the executive in order to ensure that they conform to the legal requirements and are in line with the aspirations of the people.

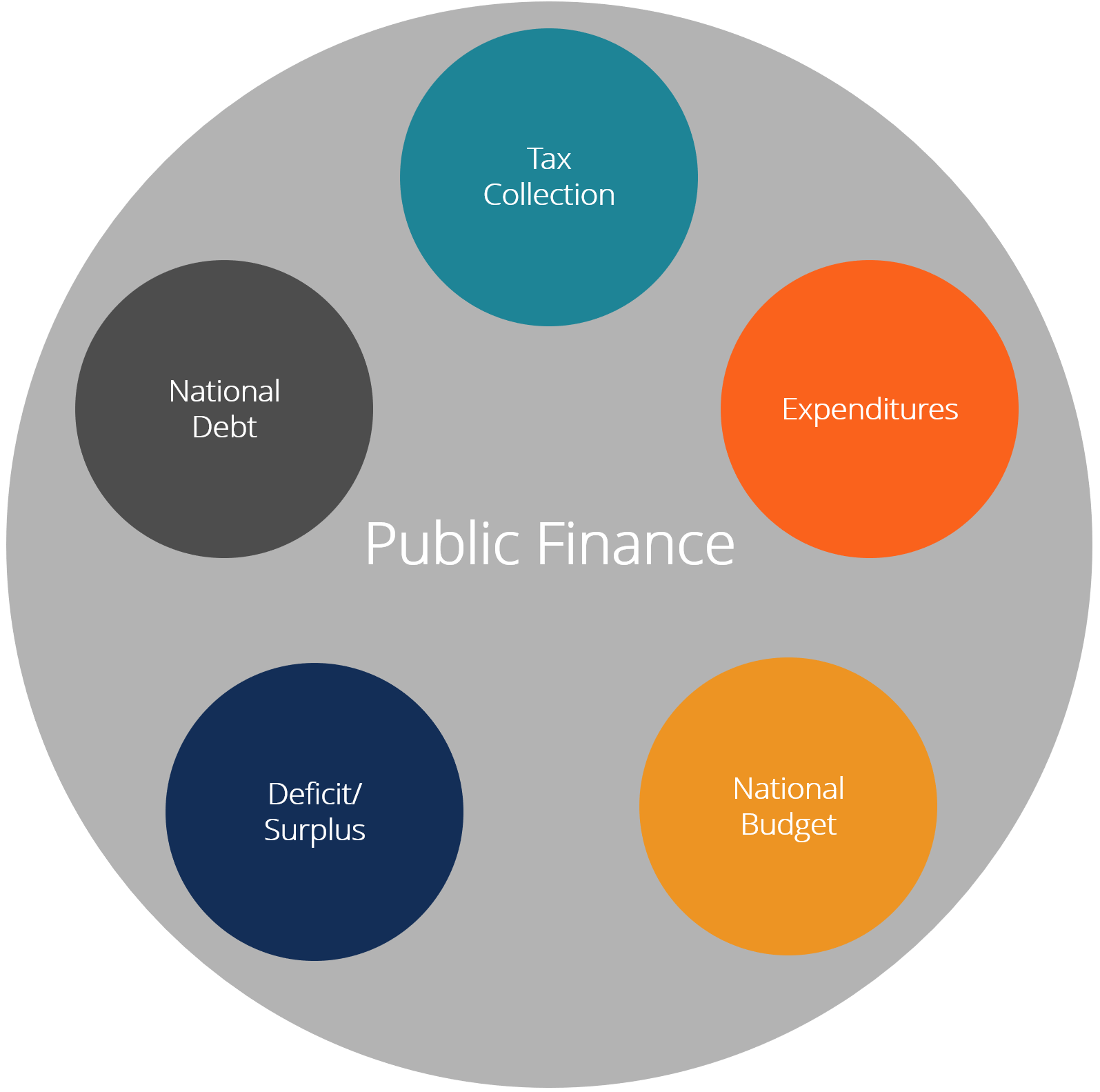

There are now numerous technical documents tabled in the assembly throughout the year that require discussion and amendment by assembly members. These documents include; the Annual Development Plan, County Budget Review and Outlook Paper, Debt Management Paper, the County Fiscal Strategy Paper and the executive budget proposal. While these documents are presented periodically to the assembly, there are also reports which should be presented quarterly, semiannually and annually on budget implementation.

All these documents require that the technical capability of the people reviewing them be above average in order to guide both the public and the county assembly. Public access of these documents from the executive still remains a challenge. My organisation’s interaction with the officers responsible for supporting county assemblies in reviewing the budget estimates suggests that these officers are facing certain key challenges, including failure by the Members of the County Assemblies to take their advice, uncooperative County Executive budget teams, and a technical skills gap.

The budget officers at the county assembly should be officers who command a lot of respect from the MCAs due to their knowledge of the budget process. While the ultimate decision to approve the budget or not rests with the Members of the County Assembly, it is critically important that the MCAs give adequate attention to these officers. The county executive budget team has unrivalled capacity at the county level in generating budget estimates and accompanying documents and also costing government programmes.

This does not however mean that county assembly budget officers should not be provided with information that they require as the purpose of these two offices should be to collectively serve the best interests of the county. While county assemblies are evolving, the technical skills gap will continue to be evident as the budget officers or fiscal analysts (as they are known) continue to transition from other fields like accounting and finance to perform these roles. Others are doubling up as auditors and accountants while playing the budget officer role.

These challenges could be resolved by having a county assembly budget office. The budget office would be an independent, objective, nonpartisan office ensuring provision of high quality research and analysis on fiscal policy directed to the county assembly. This research and fiscal analysis would be pegged on the budget cycle, but would also assess the financial implications of other executive proposals received by the legislature throughout the year. An ideal assembly budget office has six core functions which are: offering economic forecasts that are independent from the executive branch, making baseline estimates of revenues and expenditures based on current laws, analysing the executive budget proposal, developing budget projections beyond a single year and examining proposals for new programs and preparing policy briefs for existing programs.

Kenya’s Parliamentary Budget Office (PBO) was established in the year 2007 as a unit under the Directorate of Information and Research services following a resolution of Parliament. The Public Finance Management Act 2012 re-established the PBO and further enhanced its roles, thereby giving it a strong footing as a reliable institution held in high regard by the National Assembly Budget Committee in matters budgeting. The goodwill extended to the PBO by the National Assembly is a result of many years of quality work in the budget process and I believe that we should be able to witness a similar situation at the county level as devolution progresses. While there is a clear framework guiding the establishment of the Parliamentary Budget Office in Kenya, there is no such framework at the county levels, meaning that the county assemblies are potentially missing out on critical technical inputs from budget experts.

Should a county assembly budget office be established under the county assembly? I believe that counties should drive their own agenda in matters budgeting while observing constitutional principles. In Kenya, the devolved governments have been in existence for two financial years and this financial year 15/16 should present a good opportunity for counties to conduct interim assessment of the capacity of county assembly budget offices (if any exists) in terms of numbers of personnel involved, whether we have the right people serving in those budget offices, the challenges they are facing and the skills they possess. While we acknowledge the challenges being faced by the County Assemblies, the need to invest in the budget offices and provide a legal provision should form a key priority in the coming financial year 2016/17.

It will take some time to develop adequate capacities of the county assembly budget offices, but it is important for all players to understand that a strengthened county assembly budget office means effective oversight of the Executive by the County Assembly in the budget process.

Français

Français